European narrowbody aircraft fleet - the unstoppable rise of independent LCCs

Europe's six independent LCCs have 29% of all narrowbodies based in Europe, compared with 25% five years ago and 9% two decades ago.

Ryanair, easyJet, Wizz Air, Jet2.com, Pegasus Airlines and Norwegian have a combined narrowbody fleet of 1,550 aircraft. Of these, 1,215 are with the top three (Ryanair, easyJet, Wizz Air) - more than the combined narrowbody fleet of Lufthansa Group, IAG and Air France-KLM.

The low-cost brands of the three major European legacy airline groups have an aggregate narrowbody fleet of only 435 aircraft.

The independent LCCs have 1,067 outstanding narrowbodies between them, compared with 263 for the big three legacy groups (of which 103 are earmarked for their low-cost brands). The expansion of the independent LCCs' share of Europe's narrowbody fleet looks unstoppable.

Summary

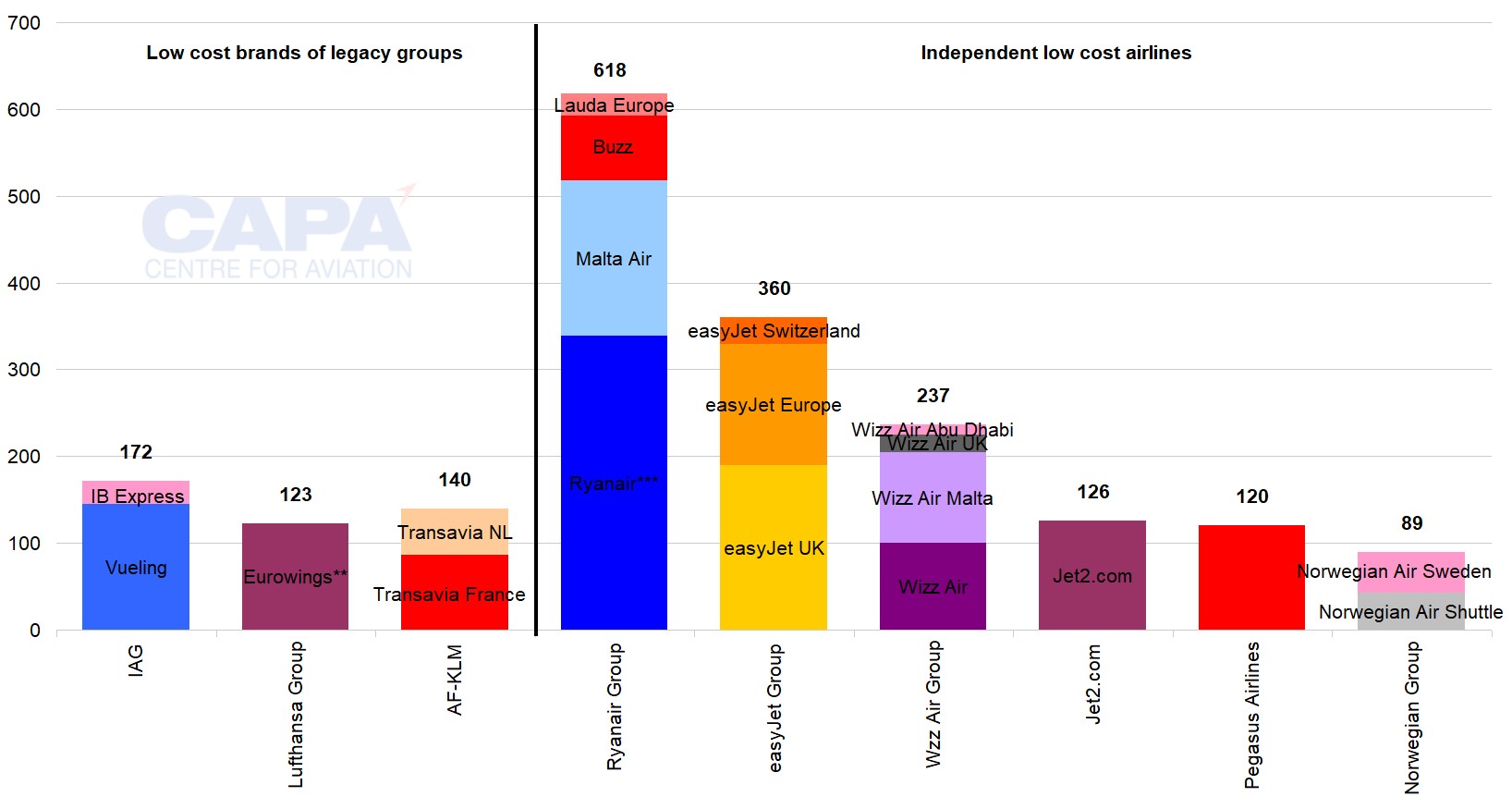

- Ryanair Group has Europe's largest narrowbody LCC fleet: 258 more than easyJet.

- Wizz Air is in a second tier all of its own, clearly ahead of third tier Jet2.com, Pegasus Airlines and Norwegian.

- The big three legacy groups have 435 low-cost brand narrowbodies and 1,196 in total, compared with the top 6 independent LCCs’ fleet of 1,550.

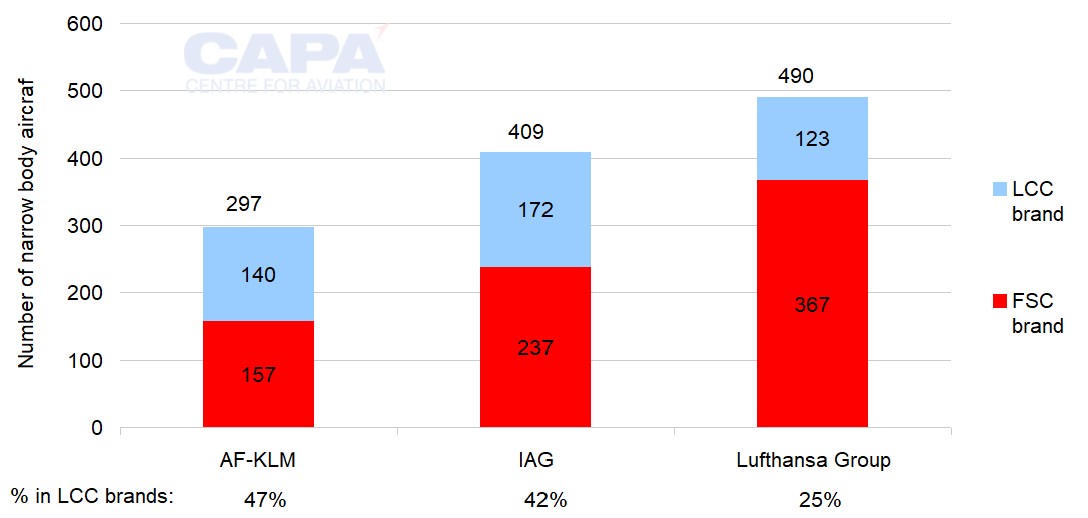

- Air France-KLM's LCC fleet is 47% of group narrowbodies, versus 42% for IAG and 25% for Lufthansa.

- The big three legacy groups have 263 confirmed narrowbody orders outstanding, versus 1,067 for the six leading independent LCCs.

- The independent LCCs' fleets will continue to grow. Ryanair is set to remain the largest, and Wizz Air could overtake easyJet by the end of the decade.

Ryanair Group has Europe's largest narrowbody LCC fleet: 258 more than easyJet

According to the CAPA - Centre for Aviation Fleet Database, Ryanair Group's total current fleet comprises 618 aircraft as at 27-May-2025. This is 258 more aircraft than Europe's number two LCC fleet, easyJet Group, which has 360.

Note that all current fleet totals in this report include both aircraft in service and inactive.

Ryanair's fleet is 72% bigger than easyJet Group's, a percentage that has increased from 34% in Nov-2019 before the COVID-19 pandemic (but is unchanged from May-2024).

Ryanair Group's fleet has grown by 173 aircraft from Nov-2019, whereas easyJet's total is only 28 aircraft more than at that time.

Wizz Air is in a second tier all of its own…

Wizz Air Group's fleet stands at 237 aircraft, which is still considerably smaller than the leading two.

However, this is 117 more than it had in Nov-2019. Before the COVID-19 pandemic, Wizz Air's fleet was not much bigger than Norwegian's, Jet2.com's and Pegasus Airlines'. At that time, all four could be considered as second tier LCCs.

Wizz Air now defines a new second tier all of its own.

Note that Wizz Air currently has 42 inactive aircraft awaiting engine maintenance, but this analysis includes grounded aircraft in the totals.

…clearly ahead of third tier Jet2.com, Pegasus and Norwegian

In the third tier, Jet2.com's 126 aircraft are 36 more than in Nov-2019. It is just ahead of Pegasus Airlines, whose 120 aircraft are 36 more than pre-pandemic.

Norwegian trails both by some distance, its 87 narrowbodies being 8 fewer than it had in Nov-2019.

European LCCs: narrowbody fleets, 27-May-2025

**Includes 29 Eurowings Europe Ltd aircraft.

***Includes 15 Ryanair UK aircraft.

Source: CAPA - Centre for Aviation Fleet Database.

The big thee legacy groups have 435 low-cost narrowbodies…

The combined narrowbody fleets of the low-cost subsidiaries of IAG, Lufthansa Group and Air France-KLM contain 435 aircraft. This has increased by 42 from a year earlier (almost half of the increase is due to Air France-KLM's Transavia).

Nevertheless, it is only 75 more than easyJet Group on its own, and 183 fewer than Ryanair Group.

The combined narrowbody low-cost fleet of the three legacy groups is 48 aircraft smaller than the aggregate fleets of Wizz Air, Jet2.com and Pegasus (483 aircraft between them).

…and 1,196 in total, compared with the top 6 independent LCCs' fleet of 1,550

Across all their airlines (low-cost and full service), the big three have a total of 1,196 narrowbody aircraft.

This compares with a total of 1,550 narrowbodies in the fleets of the six leading independent low-cost airlines of Western Europe.

The three legacy groups' LCC fleets are similar in size to the third tier independent LCCs

Individually, the size of the three legacy groups' low-cost fleets can be grouped with the third tier independent low-cost groups, albeit at the upper end of this tier.

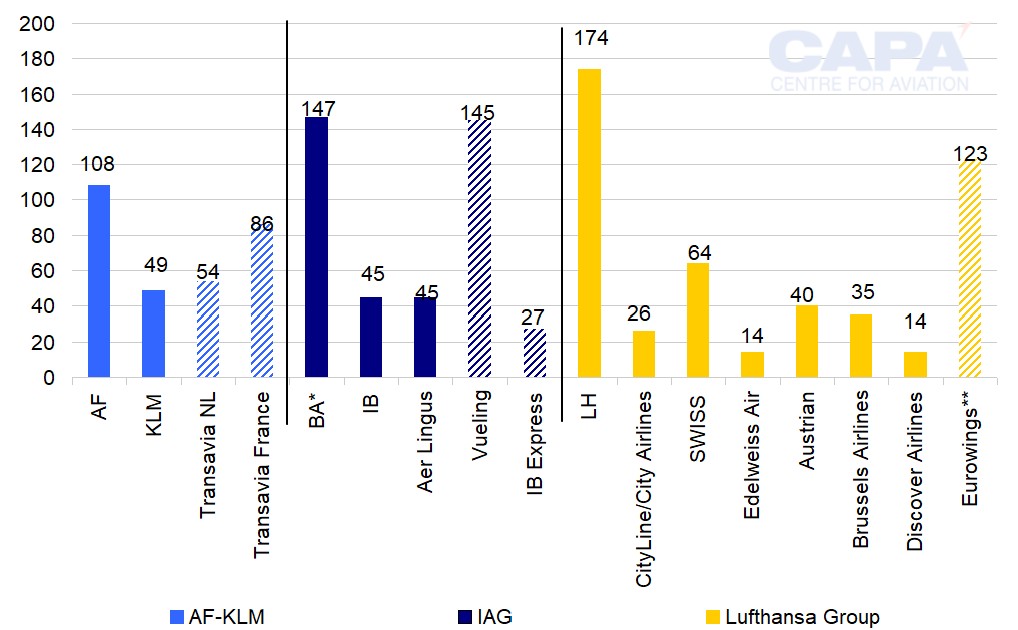

IAG has 172 low-cost narrowbodies (145 for Vueling and 27 for Iberia Express), which places it between the second and third tiers of LCC fleets in Europe.

IAG's is comfortably the biggest such fleet among Europe's big three legacy groups, and 19 more than it had in Nov-2019.

Lufthansa Group has 123 low-cost narrowbodies (94 with Eurowings and 29 with Eurowings Europe Ltd), which is 17 more than in Nov-2019.

Air France-KLM has grown its LCC narrowbody fleet the most among the three legacy groups. Its 140 aircraft (86 for Transavia France and 54 for the Dutch Transavia) are 66 more low-cost narrowbodies than in Nov-2019.

Transavia France has more than doubled from 38 aircraft in Nov-2019.

Air France-KLM, IAG and Lufthansa Group: narrowbody fleets by operator, 27-May-2025

Note: diagonal shading indicates LCC brands.

*Includes 24 BA Euroflyer aircraft.

**Includes 29 Eurowings Europe Ltd aircraft.

Source: CAPA - Centre for Aviation Fleet Database.

Air France-KLM's LCC fleet is 47% of group narrowbodies, versus 42% for IAG and 25% for Lufthansa

Although Air France-KLM's total narrowbody and LCC narrowbody fleet is considerably smaller than both Lufthansa Group's and IAG's, it has the highest percentage operated by its low-cost brands.

It has also grown this percentage the most since 2019.

Air France-KLM's Transavia brand accounts for almost half, 47%, of the group's narrowbodies - up from 29% in Nov-2019.

IAG has 42% of its narrowbodies operating with low-cost brands (only 2ppt higher than in Nov-2019), while Lufthansa Group has just 25% (down 1ppt from Nov-2019).

Air France-KLM, IAG and Lufthansa Group: narrowbody aircraft numbers by business model, 27-May-2025

Source: CAPA - Centre for Aviation Fleet Database.

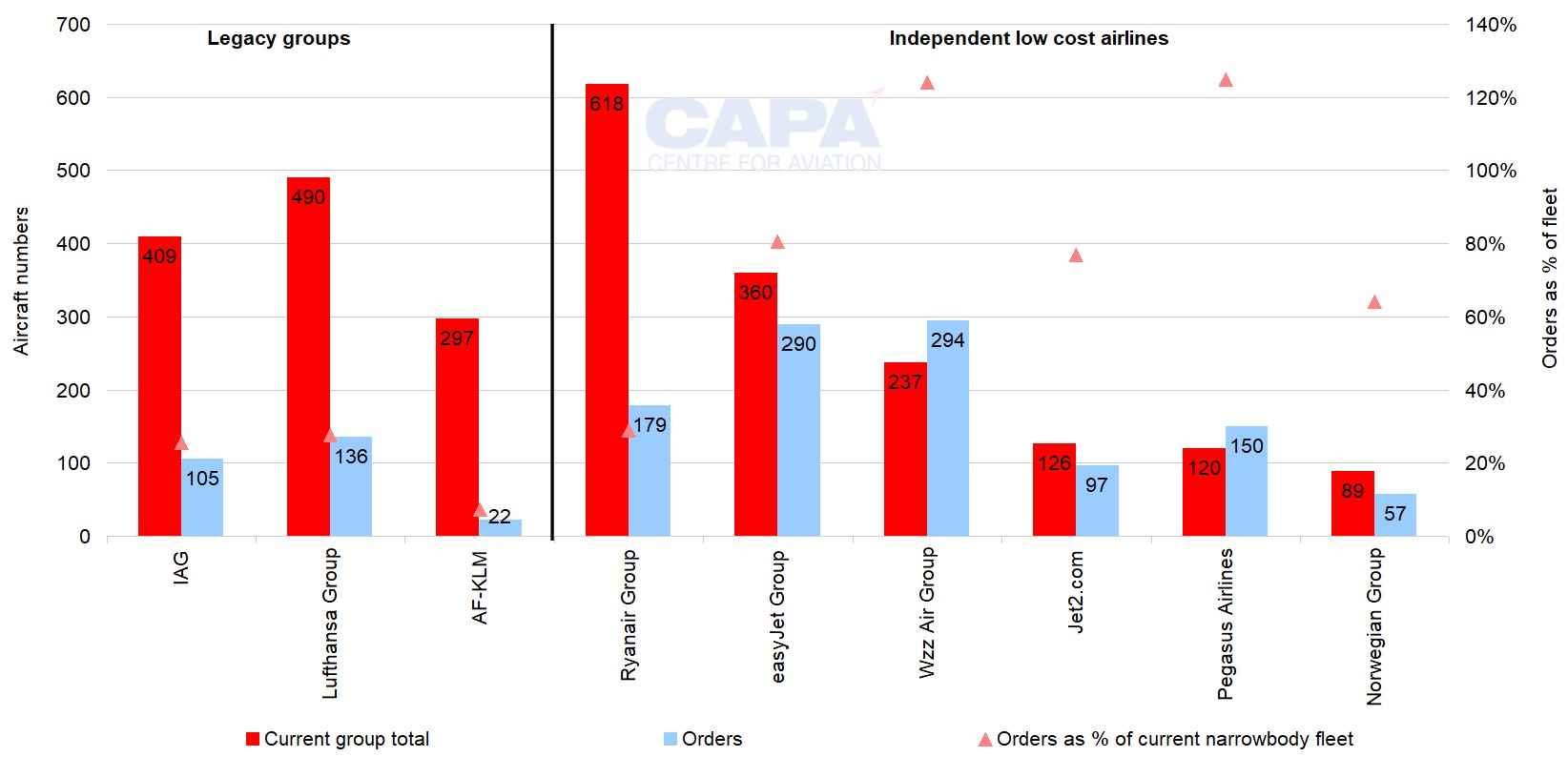

The big three legacy groups have 263 narrowbody orders outstanding…

According to the CAPA - Centre for Aviation Fleet Database, the three big legacy airline groups currently have a total of 263 outstanding orders for narrowbody aircraft.

To give some perspective, this number of orders is 60% of the total of 435 narrowbodies in their LCC brands, but only 21% of the 1,120 narrowbodies in their combined group fleets.

They have not all specified in full whether these orders are destined for their low-cost or legacy brand airlines.

However, the CAPA - Centre for Aviation Fleet Database identifies only 103 orders for the groups' LCC brands, amounting to only 24% of their combined low-cost fleet: 50 for IAG's Vueling, 48 for Lufthansa Group's Eurowings and just five for Air France-KLM's Transavia.

…versus 1,067 for the six leading independent LCCs

The six leading independent LCCs have 1,067 outstanding firm narrowbody orders between them, which is 69% of the 1,550 aircraft in their total fleet.

Between the two leading LCCs - Ryanair and easyJet - there are 469 orders, which is more than the current low-cost narrowbody fleet of the three legacy groups.

On an individual basis, Wizz Air has the highest number of outstanding firm orders, with 294 (124% of its current fleet), just ahead of easyJet with 290 (81%) and Ryanair with 179 (29%).

Pegasus has 150 orders, which is 125% of its current fleet.

Jet2.com has 97 orders representing 77% of its current fleet, and Norwegian's 57 orders represents 64% of its current fleet.

Air France-KLM has the least narrowbody orders among the legacy groups, with only 22. This is only 7% of its total group narrowbody fleet.

Its five orders identified as being for Transavia are just 4% of its LCC narrowbody fleet.

Lufthansa has 136 narrowbody orders (28% of its current group narrowbody fleet), of which 48 are earmarked for Eurowings (39% of LCC narrowbody fleet).

IAG has 105 narrowbody orders (26% of its current group narrowbody fleet), of which 50 are for Vueling (29% of its LCC narrowbodies).

European narrowbody fleets and order numbers, 27-May-2025

Source: CAPA - Centre for Aviation Fleet Database.

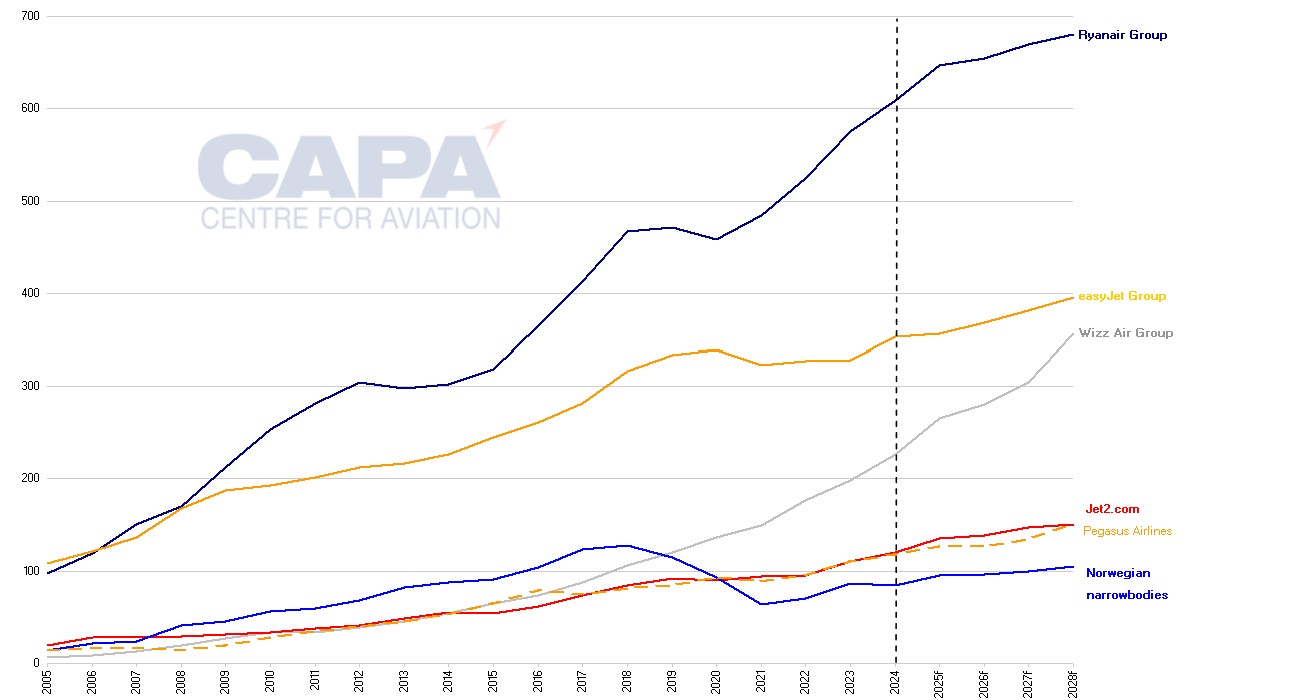

The independent LCCs' fleets will continue to grow in the coming years

The chart below shows the development at calendar year end of the leading independent LCC fleets, from 2005 to 2024. All plan further growth.

It also has CAPA - Centre for Aviation projections to 2028f, for illustrative purposes. These are based on airline company fleet plans, guidance published for financial years nearest to the calendar years of the projection, and the number of deliveries due each year (as recorded in the CAPA - Centre for Aviation Fleet Database).

Ryanair aims for 800 aircraft by the year to Mar-2034 and has published annual fleet targets until then. Its plan envisages its fleet growing to 681 in the year to Mar-2029 (closest financial year to calendar 2028).

Ryanair is set to remain the largest, while Wizz Air could overtake easyJet by the end of the decade

This will keep Ryanair comfortably ahead of all other European LCCs in terms of fleet size.

EasyJet's base case fleet plan aims for 356 aircraft in FY2025, rising to 395 in FY2027 (based on its September financial year end).

According to Wizz Air's Jan-2025 quarterly results presentation, the group plans to grow its fleet to 265 aircraft by its financial year end of Mar-2026, and to 357 by Mar-2029 (nearest to calendar 2028).

Wizz Air projects a fleet of 424 in FY2030, which is a reduction from its previous target of 451 as a consequence of supply chain problems.

Nevertheless, it should further narrow the gap to easyJet and Wizz Air, and could well overtake easyJet as Europe's number two LCC fleet by 2029 or 2030.

Jet2.com published an indicative fleet plan with its interim results presentation in Nov-2024, suggesting growth to c.151 aircraft by summer 2028 (and 163 in summer 2031).

Pegasus' 1Q20205 results presentation said it planned to have 127 aircraft at the end of 2025. The estimates in the chart below are based on expected deliveries, and allowing for some replacement, taking the fleet to 152 in 2028f.

Norwegian's 1Q2025 results presentation targets an increased to around 96 aircraft in 2026, but does not go beyond this. The chart estimates further growth to 105 in 2028f.

Ryanair Group, easyJet Group, Wizz Air Group, Jet2.com, Pegasus Airlines and Norwegian Group: year end fleet numbers 2005 to 2028f*

*Notes: historic data at calendar year end.

Source: CAPA - Centre for Aviation Fleet Database, airline reports and press releases, CAPA - Centre for Aviation estimates.

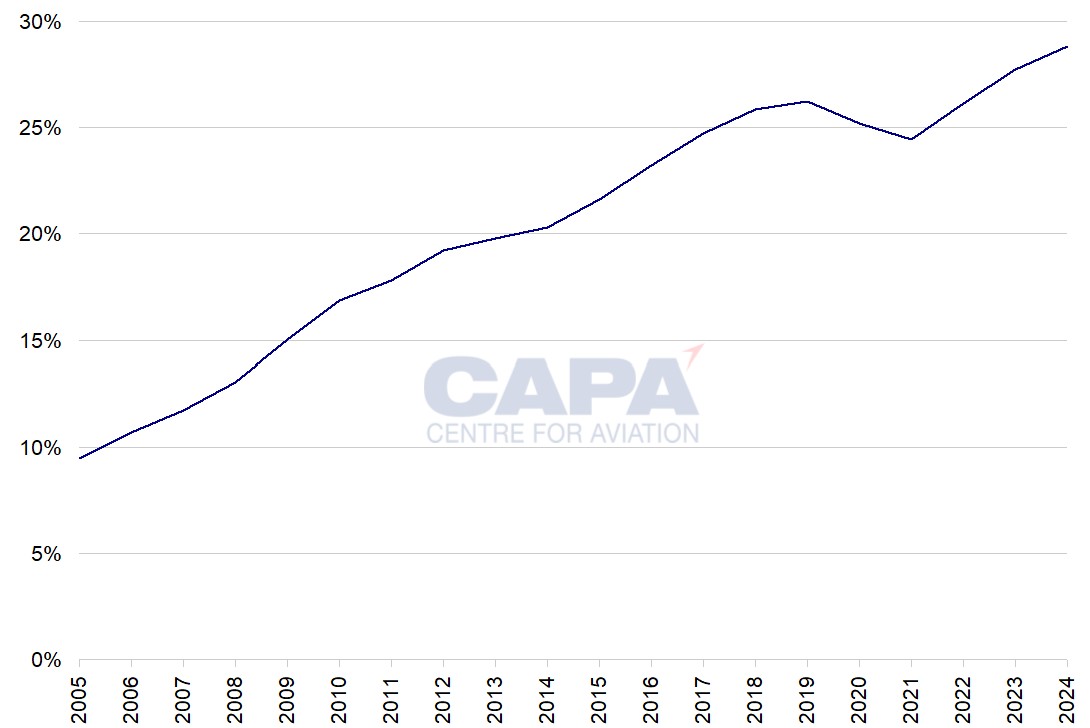

Independent LCCs share of Europe's narrowbodies is at a new high

The combined narrowbody fleets of Ryanair Group, easyJet Group, Wizz Air Group, Pegasus, Jet2.com and Norwegian Group represents 29% of the Europe's total current narrowbody fleet as at 27-May-2025.

This was an increase of more than three times from 9% at the end of 2005.

After reaching 26% in 2019, it dropped to 24% in 2021. This illustrates the independent LCCs' more flexible response to the COVID-19 crisis, when fleet growth was reversed.

Their response to the post-pandemic recovery has been equally nimble. Their share of Europe's narrowbody fleet returned to 26% at the end of 2022 and has continued to rise to its current new high level of 29%.

Their order books suggest that this share will continue to grow.

Ryanair Group, easyJet Group, Wizz Air Group, Pegasus Airlines, Jet2.com and Norwegian Group: combined share of Europe narrowbodies, year end 2005 to 2028f*

*Calendar years.

Source: CAPA - Centre for Aviation Fleet Database.