Resilient but rewritten: the new economics of air transport

The global aviation industry entered 2026 on firmer footing - but far less certain ground.

What was once a story of recovery has evolved into one of recalibration, as geopolitical fragmentation, uneven economic performance and shifting consumer behaviour begin to redraw the contours of global air travel.

This analysis examines how aviation is adapting to a world where growth is no longer uniform, predictable, or easily captured. Instead, it is increasingly shaped by regional dynamics, strategic alliances and emerging travel corridors that reflect a reordering of the global economy.

Airlines and airports must now navigate a multi-speed landscape, balancing expansion with risk, and resilience with profitability.

At the same time, structural pressures are intensifying. Sustainability commitments are moving from ambition to execution, cost bases are rising, and competition is sharpening in an environment where yields are under strain.

Meanwhile, geopolitical volatility - highlighted by recent disruptions in the Middle East - continues to expose the fragility of a highly interconnected system.

Against this backdrop, success in 2026 will depend less on scale alone and more on agility, discipline and strategic clarity. Aviation's long-term growth trajectory remains intact - but how, where, and at what cost that growth is realised is now fundamentally changing.

Summary

- Aviation in 2026 shifts from simple recovery to recalibration amid geopolitical fragmentation, uneven economics, and changing consumer behaviour.

- Growth is increasingly shaped by regional dynamics, strategic alliances, and emerging intra-regional/bloc-to-bloc travel corridors.

- The industry faces a multi-speed landscape, with stronger expansion in parts of Asia/Middle East/emerging markets and slower growth in many mature markets.

- Competition is intensifying as yields come under pressure while operating costs rise from labour, maintenance, infrastructure constraints, and sustainability investment.

- Sustainability is moving from ambition to execution, with net-zero 2050 targets proving complex and costly due to SAF availability and fleet/technology timelines.

- Middle East escalation highlights aviation’s structural exposure to geopolitical shocks, driving airspace disruptions, longer routings, higher costs, and fuel-price volatility.

The global aviation industry entered 2026 at a moment of profound transition

After several years defined by disruption, recovery and recalibration, air transport is now confronting a more complex and fragmented operating environment. The certainties that once underpinned international travel and global connectivity have weakened, replaced by shifting geopolitical relationships, evolving economic priorities and changing patterns of demand.

For airlines and airports alike, the challenge is no longer simply restoring growth, but understanding how growth itself is being reshaped.

The year ahead will be marked by ongoing geopolitical realignment, as traditional alliances are reassessed and new partnerships emerge. These shifts are influencing trade flows, tourism demand, regulatory frameworks and bilateral air service agreements, all of which directly affect airline networks and capacity planning.

As a result, air travel in 2026 is set against a backdrop of heightened uncertainty, where strategic agility and flexibility will be essential to navigating an increasingly dynamic global landscape. At the same time, aviation continues to demonstrate its resilience - the industry's ability to adapt to change, manage risk and respond to evolving market conditions remains one of its defining characteristics.

This adaptability is now being tested once again, as airlines face a multi-speed recovery, with growth patterns diverging significantly between regions and markets. Although parts of Asia, the Middle East and emerging economies are seeing robust expansion, many mature markets are experiencing more subdued demand, shaped by economic caution, demographic trends and changing consumer behaviour.

This uneven growth is accompanied by intensifying competition and mounting cost pressures. Although fuel prices have provided some relief, higher operating costs, sustainability investments and infrastructure constraints are reshaping airline economics.

In this environment, network optimisation, disciplined capacity deployment and financial resilience are increasingly central to strategic planning. For airports, these trends are equally consequential, influencing infrastructure investment, commercial strategies and long-term development priorities.

Sustainability also continues to loom large over the industry's outlook. The commitment to achieving net-zero carbon emissions by 2050 remains a defining ambition, yet the practical pathways towards that goal are becoming more complex and costly.

In 2026 the tension between environmental objectives and operational realities will sharpen, shaping regulatory approaches, airline strategies and investment decisions across the aviation value chain. And all this is occurring against geopolitical uncertainty that can force the industry to adjust overnight to challenging market conditions.

The dramatic escalation in the Middle East in late Feb-2026 has once again underlined how acutely exposed commercial aviation is to geopolitical shocks, particularly when they affect the Gulf region - one of the world's busiest air corridors.

A world in flux: from uncertainty to realignment

The year 2025 will be remembered as one of strategic ambiguity. The old global order, long anchored by predictable alliances and broadly stable economic frameworks, began to fray at the edges. In some cases, it fragmented outright. The result was a world characterised by cautious diplomacy, contested trade relationships, and increasingly regionalised economic strategies.

As the industry moves into 2026, there is a growing sense that this period of uncertainty is giving way to something more defined, though not necessarily more stable.

International relationships are being actively redefined, old alliances recalibrated, and new partnerships forged. For aviation, this geopolitical realignment is not a distant backdrop - it is a fundamental operating condition.

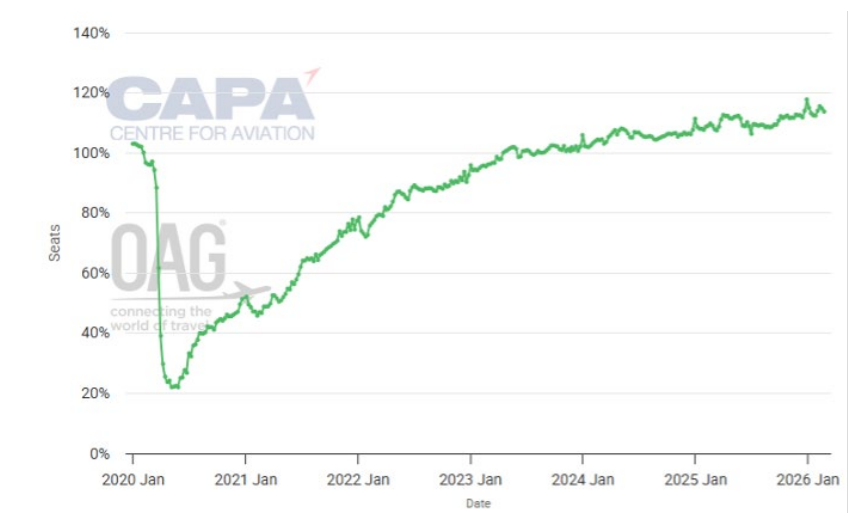

Global seat capacity versus pre-COVID baseline in 2019

Source: CAPA - Centre for Aviation and OAG.

Airlines now face a more complex matrix of political, economic and regulatory forces. Shifting relationships can quickly reshape bilateral agreements, overflight rights, visa regimes, and even passenger sentiment. The implications for air travel flows can be sudden and material.

In this environment, strategic agility is no longer a competitive advantage - it is an operational necessity.

The adaptable industry: resilience through scale and diversification

The airline industry has always demonstrated a remarkable capacity to adapt to changing circumstances. From oil shocks and financial crises to pandemics and geopolitical conflicts, aviation has repeatedly shown an ability to recalibrate and recover - that adaptability remains one of its defining strengths.

In recent years, consolidation into larger and more geographically, diversified airline groups, has added an additional layer of resilience. These groups benefit from broader network reach, more diversified revenue streams, and enhanced operational flexibility.

Importantly, this scale provides insulation from localised or regional disruptions, allowing capital and capacity to be redeployed more effectively. However, this resilience is unevenly distributed.

The largest global and regional players are best positioned to absorb shocks and capitalise on emerging opportunities.

Smaller and more geographically concentrated airlines remain more vulnerable, particularly in markets exposed to political volatility or economic weakness.

As a result, 2026 is likely to see a continued divergence in financial and operational performance across the industry

The rise of intra-regional and bloc-to-bloc travel

One of the most significant structural shifts under way is the reorientation of travel flows towards intra-regional and bloc-to-bloc markets. As geopolitical groupings realign, economic and diplomatic ties are increasingly concentrated within defined regional spheres. This is reshaping connectivity patterns and redefining growth opportunities.

Travel within regions - particularly across Asia, the Middle East, parts of Africa, and Latin America - is expanding rapidly. At the same time, traffic between aligned blocs is showing renewed momentum, driven by trade, investment and strategic cooperation.

This is not merely a cyclical rebound. It reflects deeper changes in global economic geography, supply chain localisation, and diplomatic alignment.

For airlines, this means that future growth will be less evenly distributed and more dependent on strategic positioning within these emerging corridors.

Long haul international travel remains resilient, but its growth profile is changing. Demand is becoming more selective, more price-sensitive, and increasingly influenced by geopolitical perceptions.

Network strategies in 2026 will need to be both opportunistic and cautious, balancing expansion with risk management.

A multi-speed world: uneven recovery and divergent growth paths

The aviation landscape in 2026 has a distinctly multi-speed character. Some regions and markets are racing ahead, while others struggle to regain momentum. Developing economies - particularly those that view aviation as a cornerstone of national development strategies - are leading the charge.

Investments in infrastructure, liberalised market access, and tourism promotion are translating into robust traffic growth. In these markets, air travel is seen as an economic catalyst rather than a discretionary luxury.

In contrast, many mature markets, especially large domestic markets and advanced economies, appear to be stuck in a prolonged period of stagnation. This reflects a combination of post-pandemic normalisation, demographic headwinds, and cautious consumer sentiment.

While traffic volumes remain substantial, growth rates are subdued, and competitive pressures are intensifying. Some of this slowdown is inevitable. The extraordinary rebound that followed the COVID-19 pandemic was always unsustainable.

As travel patterns normalise, growth is reverting to long-term averages. However, there are also cyclical and transitory influences at play, including supply chain disruptions, inflationary pressures, and shifting consumer priorities.

Structural shifts: redefining long-term growth

Beyond short-term cycles, a more profound structural shift is under way.

The era of consistently high growth that characterised much of the pre-pandemic period is unlikely to return in its previous form. Demographic trends, particularly in developed economies, are moderating demand growth. Economic uncertainties, higher living costs, and increased sensitivity to environmental concerns are further reshaping travel behaviour.

At the same time, geopolitical fragmentation is altering traditional connectivity patterns and constraining network expansion.

Environmental considerations are becoming an increasingly influential factor.

Regulatory frameworks, public expectations, and investor scrutiny are converging to impose higher costs and greater complexity on airline operations.

While sustainability initiatives remain central to the industry's narrative, the pathway to net-zero emissions by 2050 is proving to be far more challenging than initially anticipated. The available levers - sustainable aviation fuels, fleet renewal, operational efficiencies, and emerging technologies - are all progressing, but at a pace and scale that struggle to match the ambition of stated targets.

Moreover, these initiatives come with substantial financial implications, placing additional pressure on margins in an already competitive environment.

Intensifying competition: yields under pressure, strategy under scrutiny

As growth moderates, competition is intensifying. Fare growth is slowing, yields are under pressure, and capacity deployment is becoming more strategic.

While fuel prices have remained stable for a couple of years providing some relief, this has been offset by higher labour, maintenance and infrastructure costs.

In this environment, cost containment, network agility and strategic flexibility are becoming paramount.

Airlines are increasingly focused on optimising fleet utilisation, refining route portfolios, and enhancing revenue management capabilities.

Ancillary revenues, loyalty programmes and partnerships are playing a more prominent role in sustaining profitability.

The competitive landscape is steepening, with weaker players facing mounting challenges.

This is likely to accelerate consolidation in certain markets, particularly where regulatory environments allow.

Strategic alliances and joint ventures will also continue to evolve, offering pathways to scale and market access without full mergers.

Cautious consumers: changing travel behaviour and spending priorities

Consumer sentiment entering 2026 is marked by cautious optimism.

While there remains a strong desire to travel - particularly internationally - this is tempered by heightened sensitivity to personal finances and broader economic conditions.

Travellers are becoming more selective in their destination choices, timing, and spending patterns. Value for money, flexibility, and perceived safety, are increasingly influential factors.

This is driving demand for off-peak travel, alternative destinations, and more nuanced product offerings.

For airlines, this necessitates a more sophisticated approach to pricing, distribution and customer engagement.

The ability to anticipate and respond to rapidly shifting demand signals will be a critical determinant of success.

Sustainability: ambition meets operational reality

As financial stability improves across much of the industry, sustainability has re-emerged as a central strategic concern. The bold commitment to achieve net-zero emissions by 2050 remains intact, but the practical challenges are becoming more evident.

The cost and availability of sustainable aviation fuels, the pace of fleet modernisation, and the development of new propulsion technologies all pose significant hurdles. At the same time, regulatory expectations and public scrutiny are intensifying.

In 2026 sustainability will increasingly shift from aspirational commitments to operational execution. Airlines will be required to demonstrate tangible progress, even as they grapple with the financial and logistical implications.

This balancing act will shape strategic decision-making across the sector.

Geopolitical shockwaves: the Iran escalation and aviation's structural exposure

Events in the Middle East have quickly evolved from a regional security crisis into a systemic disruption for global aviation. What initially appeared to be another episode of Middle East volatility has instead highlighted the extent to which modern air transport depends on a narrow geographic corridor linking Europe, Asia and Africa.

These events underline that the disruption is not simply a short-term operational challenge but a structural stress test for the industry. The Gulf region has become one of the world's most critical aviation crossroads, connecting long haul flows between Western Europe, South Asia, Southeast Asia and Australasia. When that corridor is constrained, the effects quickly propagate across the global aviation system.

The crisis has also brought renewed scrutiny to the Gulf hub model. These hubs rely on uninterrupted airspace access and efficient transfer connectivity. The disruption highlights how concentrated global connectivity in a geopolitically sensitive corridor can create potential single points of failure.

Operationally, airlines are already experiencing higher fuel burn, longer flight times and reduced aircraft utilisation as flights detour around restricted airspace. Economically, the impact extends beyond immediate cancellations. Elevated war-risk insurance premiums, higher operating costs and disrupted network planning are placing additional pressure on long haul route economics.

In this sense, the Iran escalation represents more than a temporary disruption. It is a reminder that the global aviation system, optimised for efficiency and connectivity, remains inherently exposed to geopolitical shocks. The industry's ability to adapt to this new operating reality will be a defining factor in its resilience over the coming decade.

Fuel market volatility: the rising cost of geopolitical risk

Beyond airspace disruption, the escalation around Iran also carries significant implications for global fuel markets and airline economics.

The Middle East remains one of the world's most strategically important energy regions, and geopolitical instability in the area tends to translate rapidly into oil price volatility. Even modest increases in crude oil prices can have an outsized impact on airline finances, as fuel typically represents one of the largest components of operating costs.

Heightened tensions in the region have already begun to introduce uncertainty into energy markets, driving price fluctuations and increasing hedging complexity for airlines. Should the conflict expand or persist, upward pressure on oil prices could intensify, raising the cost of jet fuel globally and directly affecting airline margins.

For the global aviation sector, rising fuel prices linked to geopolitical tensions represent a familiar but potent challenge. When combined with disrupted airspace and longer routings, they amplify the economic consequences of conflict well beyond the immediate region.

The ability of airlines to manage this risk through hedging strategies, operational efficiency and network flexibility will be a key determinant of financial performance in the months ahead.

Looking ahead: cautious confidence in a complex world

The aviation industry entered 2026 with a sense of cautious confidence. The uncertainties of 2025 may be receding, but they are being replaced by a more complex and fragmented global environment. Growth remains intact, but its character is changing. Competitive pressures are intensifying, and strategic choices are becoming more consequential.

Yet, the industry's inherent resilience, adaptability and innovative capacity should not be underestimated.

Airlines have repeatedly demonstrated an ability to navigate turbulent conditions, recalibrate strategies, and emerge stronger.

As has already been seen, 2026 will undoubtedly present its own unique complications. But for an industry that thrives on movement, connectivity and transformation, these challenges also represent opportunities.

The upward trajectory of aviation is holding - for now. The task ahead is to ensure that this momentum is sustained in a world that is being fundamentally reshaped.

DOWNLOAD CAPA - Centre for Aviation's 'Aviation in 2026 - The CAPA Perspective' report

Against this backdrop, CAPA - Centre for Aviation's 'Aviation in 2026 - The CAPA Perspective' report provides a high-level perception on the forces shaping global air travel over the year ahead. It highlights the key factors influencing airline and airport performance, examines regional dynamics and market-specific trends, and assesses how strategic priorities are evolving in response to geopolitical, economic and environmental change.

The report also offers CAPA - Centre for Aviation's outlook for major regions and individual markets, alongside dedicated insights into the airport sector, where capacity constraints, infrastructure investment and commercial diversification are becoming increasingly critical.

Together, these perspectives aim to provide a clear, balanced and forward-looking assessment of the opportunities and risks facing the aviation industry in 2026, at a time when navigating fragmentation and realignment has become central to sustaining growth.