VietJet looks to dip its toe into the Australian domestic market – but faces significant hurdles

A proposal by VietJet Group to establish a new Australian-based carrier raises the question - once again - as to whether a third jet operator can survive in the Australian domestic market.

VietJet obviously believes the answer is yes, and so do another couple of potential startups that are interested in launching in Australia.

The challenges are huge, but that will not stop people thinking they have the business model to succeed where others have failed.

The regulatory and political environment may be conducive to such efforts, as there is a prevailing attitude that Australia needs more competition.

But even if they gain approval, the much larger question is whether they can be sustainably viable.

Summary

- Clues emerge that VietJet Group is looking to start up a domestic carrier in Australia with 10 Boeing 737 MAXs.

- VietJet would have to take on dominant incumbents Qantas, Jetstar and Virgin Australia on domestic jet routes.

- The failures of Rex’s jet operation and Bonza in recent years highlight how difficult it is for startups in this arena.

- Koala Airlines and Zinc are other proposed startups looking to put their hat in the ring in Australia.

- Building a successful new entrant in Australia will take time, patience and probably significant investment.

Details have begun emerging about VietJet Group's proposal for Australian startup, but no confirmation from the airline yet

The rumour about VietJet Group's interest in Australia has been floating around for some time, although it became much more solid when the Australian Financial Review reported that the carrier had applied for an air operators' certificate (AOC) there.

The Civil Aviation Safety Authority (CASA) has stressed that it does not comment on airlines' commercial plans, and VietJet has yet to confirm the report.

But industry sources have stated that the AFR report is generally correct and the AOC application process has been started.

Previously, the Analytic Flyer website noted that an unnamed airline had been allocated slots at Sydney Airport for the upcoming Northern Winter season starting in Oct-2026. This airline is now known to be VietJet.

Of course, the startup would still need an AOC before using any of the slot allocation.

CASA typically takes 6-12 months to consider an AOC application, assessing technical and safety factors as well as financial viability.

Unlike many other countries, Australia has very liberal ownership laws allowing foreign entities to set up and own carriers for domestic operations.

According to the AFR report, VietJet proposes starting with 10 Boeing 737s.

The VietJet Group parent company operates an all-Airbus narrowbody fleet, but it also has about 150 Boeing 737-8s and the high-capacity 737-8200s order (in addition to 186 A321neos).

Subsidiary Thai VietJet operates a mixed narrowbody fleet including 10 737-8s with another 39 remaining on order, according to the CAPA Fleet Database.

VietJet's Kazakh subsidiary operates a small fleet of turboprops.

The parent VietJet carrier already serves Australia, with routes from Vietnam to Brisbane, Melbourne, Perth and Sydney.

The new entrant will not be able to avoid competition with the dominant incumbents

The description of the Sydney slots VietJet has been allocated indicate they would be sufficient for seven daily return services.

Assuming the carrier would be flying narrowbody jets domestically, it is likely targeting trunk routes between the state capitals, particularly the so-called Golden Triangle routes between Sydney, Melbourne and Brisbane.

To start international services (i.e. to New Zealand or Southeast Asia short-haul leisure destinations), the carrier would need ownership and control to be held by an Australian partner.

So this means VietJet will probably be going head-to-head against Qantas Group and Virgin Australia on domestic trunk routes.

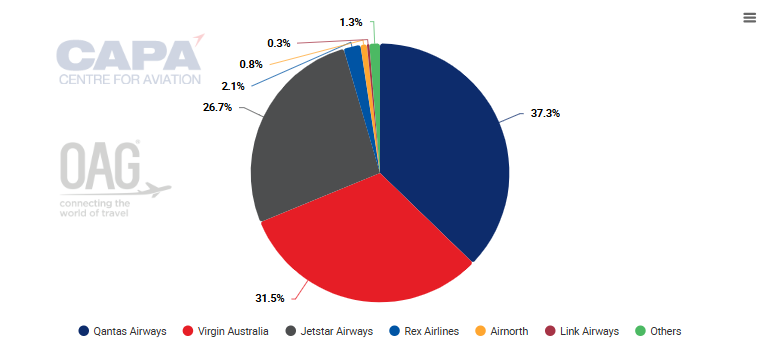

The chart below shows that Qantas is the dominant domestic competitor with 37.3% of weekly seats, or 64% when including Jetstar.

Virgin Australia accounts for 31.5%, and the other minor players are regional operators.

Australian domestic capacity by carrier, as measured by departing seats for the week of 29-Jun-2026

If there were any non-served domestic routes that would be profitable with 737s (or A320s), then one of the incumbents would likely be operating them.

So the question for VietJet (or any other challenger) is how do you overcome the frequency, network and loyalty programme advantages of Qantas and Virgin Australia?

VietJet will likely seek to operate a low-cost model like the parent carrier. But gaining a cost advantage is not as simple as it might seem, as Australia is a relatively high-cost operating environment, and the newcomer would take time to build scale efficiencies.

Rex and Bonza examples highlight how difficult it is to survive as a subscale startup

Any talk of a new entrant to the Australian domestic market will obviously raise the spectre of the two recent failed efforts.

Longtime regional carrier Rex attempted to branch out beyond its turboprop services by starting a narrowbody jet operation on Australian trunk routes in 2021.

This service eventually covered a handful of routes between state capitals with nine aircraft.

However, the fleet did not grow anywhere near as quickly or as much as the carrier envisaged.

The narrowbody operation struggled to breakeven and played a major role in the Rex entering voluntary administration in Jul-2024, when the narrowbody operation was dumped (as this CAPA - Centre for Aviation analysis discussed).

Rex believed there was an opportunity in the market due to the retreat of the incumbents in the aftermath of the COVID-19 pandemic, but the opening was short-lived as the incumbents bounced back.

Bonza, meanwhile, started in Jan-2023 with a business plan of operating Boeing 737 MAXs on domestic routes that were either unserved or underserved.

But Bonza was also forced to pull the plug in Apr-2024 when its overseas owner essentially withdrew support. The carrier was operating just five narrowbodies when it ceased operations (as this CAPA - Centre for Aviation analysis described).

So recent history has not been kind to new entrants in Australia.

Something Bonza and Rex's jet operation had in common was that they did not survive long enough to achieve the scale they would have needed to compete effectively in the Australian domestic market.

VietJet is not the only one eyeing the Australian domestic market, with Koala and Zinc touting their concepts

The experiences of Rex and Bonza have not stopped more potential challengers from looking to try their luck in the Australian market.

Koala Airlines is a proposed startup that intends to lease 737-8s for use on domestic trunk routes.

Koala says it has an AOC previously used by another operation, but it does not cover the aircraft it wants to fly. So it will have to work with CASA to gain certification.

The carrier says it is working on the documentation required by CASA, but it is unclear how advanced this process is and there appears to be no firm timeline.

Another proposed new entrant is Zinc, which like Koala is being promoted by an airline industry veteran.

Zinc aims to operate as an ultra-low-cost carrier (ULCC) using Airbus A321neos on domestic trunk routes.

However, Zinc says a major point-of-difference is that it will use the new Western Sydney International Airport rather than the congested main Sydney Airport.

The advent of WSI means the airline "can access the Sydney market without the constraints that have defined - and defeated - every previous challenger," according to Zinc's marketing pitch.

The carrier is believed to be still seeking investment, and again no firm launch timetable has been revealed.

Australian startup investors would need deep pockets and lots of patience

It is still not certain that VietJet will follow through and actually launch an Australian operation, and the carrier is keeping its cards close to its chest for now.

However, it does appear to be further along the development and approval curve than the other two prospective new entrants.

Even after launch, they would all face many hurdles to become the sustainable, viable, long-term operations they envisage.

What it will take is the considerable financial backing and patience required to support a nascent carrier while they build to breakeven scale.

It may also take time to win the confidence of the traveling public, and to overcome the brand, loyalty programme, network and frequency advantages of the Qantas Group and Virgin Australia.

The VietJet parent brings some considerable backing, of course. But it would have to be prepared to absorb startup losses in the subsidiary's early years.

The Australian market obviously remains a tantalising prospect for newcomers who believe they have the right formula to crack it where others have failed.

For VietJet, there would be broader appeal; an Australian operation would be part of a wider group with entities in different parts of the Asia Pacific region.

The advantage to such an approach is that it spreads the risk of relying too much on one geographic market, and investment can be funnelled to the entities that are seeing the greatest returns.

It also helps build group-wide scale, giving the parent company options of where to deploy its massive narrowbody order backlog and will build feed into its widebody international network.