Under the microscope: US airlines confront pricing and and demand doubts ahead of earnings

US airlines are preparing to kick off second-quarter earnings season, and one of the biggest questions facing management teams is whether strong demand and recent fare increases will prove durable through the remainder of the year.

Unsurprisingly, airline stocks rallied after the US and Iran unveiled a memorandum of understanding in early Jun-2026, aimed at paving the way for a broader peace agreement. As oil prices eased, the prevailing view was that airlines would be able to maintain higher fares because demand remains strong while industry capacity has been trimmed.

But beyond that headline conclusion, does a potential easing of geopolitical tensions provide any additional clarity into how airlines plan to navigate the back half of the year?

As executives prepare for earnings season, they're likely refining their answer to that question.

Summary

- US airlines head into 2Q2026 earnings with the key question of whether demand strength and recent fare increases will hold through the rest of the year.

- Airline stocks rose after a US-Iran memorandum of understanding eased oil prices, supporting the view that carriers can sustain higher fares amid trimmed capacity.

- United Airlines CEO Scott Kirby flagged potential fare elasticity even as United implements a major 5% capacity cut in 2026 to improve supply-demand balance.

- Industry capacity is not uniformly shrinking, with CAPA - Centre for Aviation/OAG data showing US domestic ASMs slightly elevated in 2H2026 and international ASMs rising again from late Sep-2026.

- Delta Air Lines' and Southwest Airlines' leadership express confidence that bookings remain resilient and that the industry will avoid giving back fare increases, citing strong leisure and business demand.

- Despite improved fuel and pricing dynamics, airlines face structurally thin margins, IATA has cut its 2026 net margin forecast to 2.0%, and geopolitical/policy volatility remains an overhang.

Will US capacity need to drop further to ensure fare increases stick?

Even before negotiations toward a peace agreement began, some airline executives were commenting about fare elasticity.

Speaking at the IATA Annual General Meeting in early Jun-2026, before the US-Iran ceasefire, United Airlines' CEO Scott Kirby said, "I expected a bigger elasticity effect than we've seen so far… I still do expect it, by the way."

United has initiated one of the largest capacity cuts among US airlines - 5% for 2026 - to create a favourable supply-demand scenario.

Other airlines appear to be waiting until the busy summer season is over to determine their capacity plans.

See related CAPA - Centre for Aviation report: Carriers tout strong demand amidst fare increases, but price elasticity is inevitable.

Logic would dictate that additional capacity reductions should ensue to keep fare increases in place.

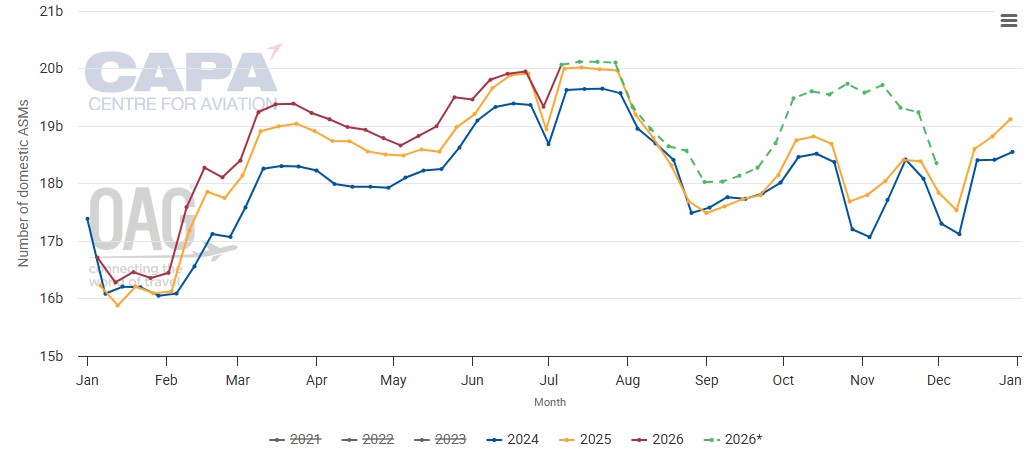

Data from CAPA - Centre for Aviation and OAG show US domestic capacity measured by available seat miles (ASMs) is expected to remain slightly elevated in the back half of year.

United States of America: weekly total domestic available seat miles from Jan-2024 to 30-Nov-2026

Source: CAPA - Centre for Aviation and OAG.

* These values are at least partly predictive up to 6 months from 29-Jun-2026 and may be subject to change.

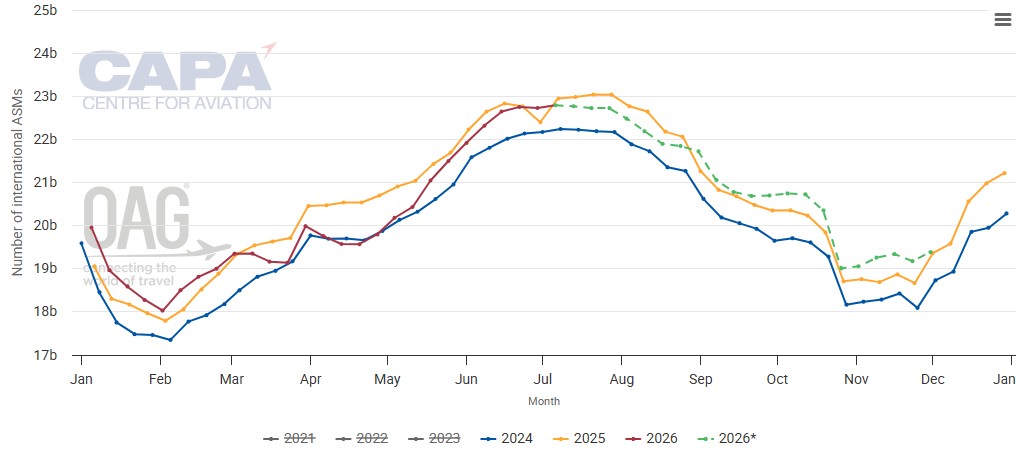

International ASMs are just slightly lower in the summer season before inching up in late Sep-2026, reflecting a trend that's emerged during the last few years of higher demand in what was historically considered shoulder periods.

United States of America: weekly total international available seat miles from Jan-2024 to 30-Nov-2026

Source: CAPA-Centre for Aviation and OAG.

* These values are at least partly predictive up to 6 months from 29-Jun-2026 and may be subject to change.

Delta and Southwest exude confidence regarding market conditions as demand holds steady

Perhaps offering a preview into upcoming commentary regarding supply and demand, Delta CEO Ed Bastian recently told Fox Business that after the initial oil shock tickets prices increased broadly 10%-15% across the industry. "I think that was probably the right level, oil prices have come down now, so I think we're in a pretty good spot."

Mr Bastian also told the media outlet that bookings have continued to be very resilient even with fare increases necessitated by higher fuel costs. "As we get out into the Fall, I expect the full year's going to be really healthy."

Before the US-Iran MoU, Southwest's leadership struck a confident tone, arguing that the industry has a vested interest in maintaining higher fares.

"We and our competitors are all focused on ratable production of results, steady production of results, sustainable margins, and so I do think that produces a backdrop where we'll certainly not attempt to give some of these fare increases back," Southwest CEO Robert Jordan said.

Mr Jordan also pointed to continued resilience among both leisure and business travellers, across geographies and throughout the booking curve.

"The consumer remains very strong, despite this rise in fares, so I'm becoming increasingly bullish that we will be able to cover these fuel increases with revenue increases," he said.

Even with confidence of solid demand remaining in place, razor thin airlines for margins persist

Airlines are doing and saying all the right things to ensure higher fares persist through the remainder of the year.

For now, they remain positive about the prospects of fare increases remaining in place. US airlines are also benefitting from the exit of ultra-low cost carrier Spirit Airlines from the market, which removed some bottom level fares in the market.

Ultimately, however, consumers will determine whether pricing holds, and predicting traveller behaviour remains difficult. Additionally, further fare increases are a non-starter now that fuel prices have fallen.

There is also a reality that falling fuel prices cannot solve: the industry's already-thin profit margins continue to come under pressure.

IATA recently revised its 2026 profitability forecast for global airlines, lowering expected net margins for 2026 from 4.2% to 2.0%, and cutting projected industry profits nearly in half.

Even if the current US-Iran truce evolves into a permanent resolution, volatility is unlikely to disappear.

At the start of the year, few anticipated a Middle East conflict that would send airline fuel costs sharply higher. Yet those events unfolded during the first half of 2026, underscoring how quickly industry assumptions can change.

Even as the US and Iran work towards a peace deal, uncertainty prevails

Although falling fuel prices and the belief that increases in fare are sticking are welcome news for investors, there's an argument to be made that uncertainty remains an overhang for the second half of the year.

In Jan-2026, Mr Bastian observed: "I think, relative to the [Trump] administration and their priorities, I think we're all one year smarter and more conditioned to expect maybe the unexpected in some of the policy approach".

Nearly halfway through 2026, that observation resonates more than ever.