Global air travel growth faces limitation from slow aircraft deliveries

CAPA ANALYST PERSPECTIVE - a new series where CAPA - Centre for Aviation's analyst team provide personal views on a hot topic facing aviation around the world. Air travel has now returned to pre-pandemic levels and forecasts are that growth in passengers will continue into 2024, albeit moderating somewhat from recent rapid growth. The outlook for the air transport sector is now largely positive, with airlines and airports reporting record revenue and the sector largely moving back towards profitability, after a series of difficult years. However, if you look at the state of the global aircraft manufacturing industry, a very different picture emerges. You might even be forgiven for thinking that the crisis induced by the COVID pandemic has yet to end. Simon Elsegood, Head of Research at CAPA - Centre for Aviation shares his viewpoint.

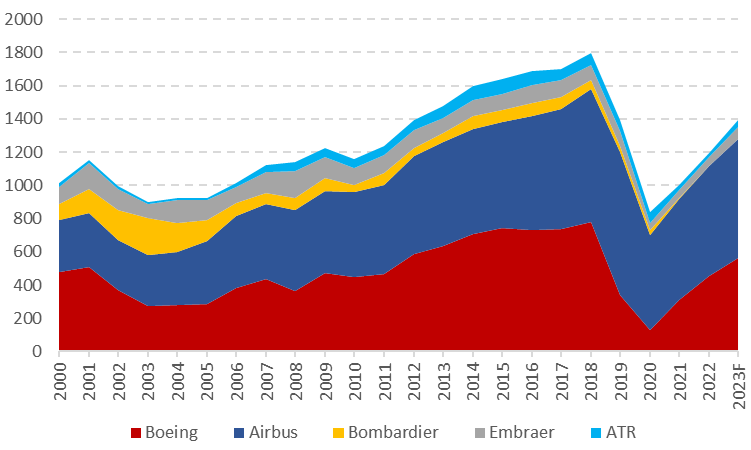

Aircraft deliveries dropped sharply after 2018, due to 737 MAX grounding and then COVID-19

Aircraft deliveries by the major western aircraft makers – Airbus, Boeing, Embraer and ATR – dropped sharply after 2018, thanks to the combination of the global 737 MAX grounding and then the COVID-19 pandemic.

With air travel at a near standstill, western original equipment manufacturers (OEMs) cut output sharply and reversed plans to increase production capacity.

As a result, aircraft deliveries in 2020 were less than half of the pre-pandemic.

Commercial aircraft deliveries by western OEMs (2000-2003F*)

Source: CAPA – Centre for Aviation & company reports.

*2023 forecast based on manufacturer’s upper estimates.

While OEMs have managed to rebuild deliveries since then, output is still well below where their customers want it to be.

Even if the four major OEMs manage to meet their most ambitious output targets for 2023, deliveries will still only be approximately three quarters of the pre-pandemic peak.

The European manufacturer Airbus is broadly on track to meet its 2023 delivery target of 700-720 aircraft – although this is up from the 661 the previous year, this is also only the same level of output the OEM was targeting for 2022.

Airbus has ambitious plans for production ramp-ups, although ongoing dislocation in the aerospace sector’s complicated and interdependent global supply chain continues to frustrate its ambitions.

The OEM plans to increase production across its entire aircraft roster, from a nominal 59 per month at present to as many as 102 per month by the end of 2023.

Central to this is the A320neo family, whose production will be raised from 45 to 75 per month over a three-year period.

However, issues with the PW1100G-JM engine, which powers around 40-45% of the A320neo family fleet, could have a significant impact on the OEM’s plans.

Due to a flaw with powdered metal parts used in the engine discovered by the engine maker Pratt & Whitney, around 1800 to 1900 engines will need to be removed from A320 family aircraft for inspections between 2023 and 2026.

With each engine taking somewhere between 250 and 300 days to remove from the wing, inspect and then reinstall, Pratt & Whitney estimates an average of 350 aircraft will trapped on the ground every day between 2024 and 2026.

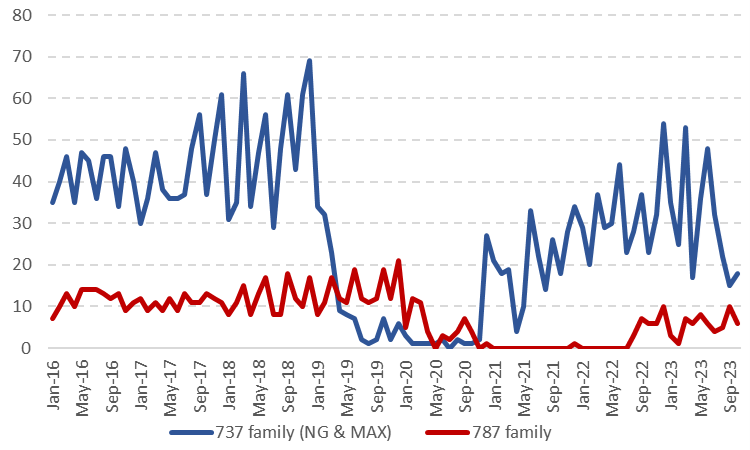

Boeing’s performance has not been any better.

Deliveries from the US aircraft maker for the first 10 months of 2023 were 395 aircraft, which is an increase of a modest 8% year-on-year.

Boeing remains in the grip of crises involving its two most numerically and financially important aircraft programmes – the 737 MAX narrowbody and the 787 widebody.

As of the end of 3Q2023, there were approximately 250 737s ‘in inventory’ with Boeing, along with another 75 787s, as the OEM completes fixes and reworks to deal with a number of production issues.

Boeing hopes to have the grounded 787s to customers by the end of 2024, while deliveries of the 737 MAX aircraft that Boeing has in inventory are expected to continue into 2025.

Boeing 737 family and 787 family deliveries (Jan-2016 to Oct-2023)

Source: CAPA – Centre for Aviation & company reports.

Compounding this is the discovery of ‘non-conforming holes’ in the aft pressure dome of certain 737 MAX aircraft. While Boeing is working with the fuselage supplier Spirit AeroSystems to rectify this, the OEM has cut its delivery outlook for the narrowbody from 400-450 aircraft to 375-400 aircraft.

The issue has also impacted production of newly built aircraft, slowing Boeing’s planned rate transition from 31 per month to 38 per month from mid-2023 to late 2023.

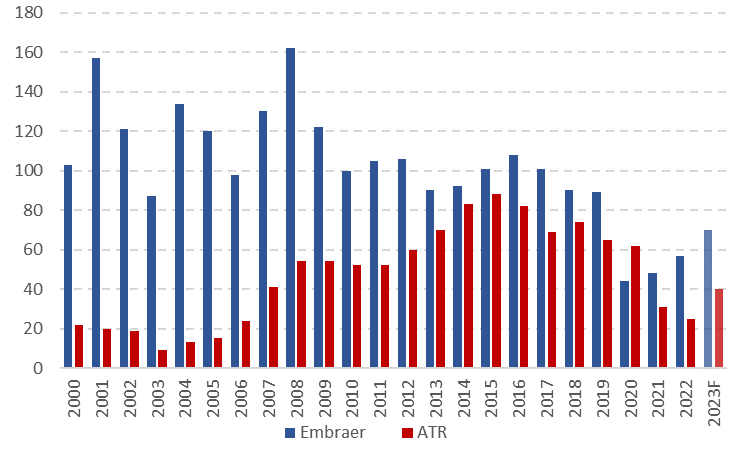

One of the few bright spots for the sector lies with smaller aircraft makers Embraer and ATR.

Output at the Brazilian regional jet manufacturer Embraer is expected to reach 65-70 aircraft – up from 57 in 2022.

Embraer is working towards building production rates back up beyond 100 aircraft per year, although the OEM’s firm order book of just 291 aircraft could act as a spoiler of these ambitions.

ATR is aiming to deliver a minimum of 40 aircraft for 2023, after producing just 25 in 2022. The Franco-Italian turboprop market has ambitions to ramp up production to 80 aircraft per month. This would result in it matching delivery levels from broadly a decade ago although, as with Embraer, there are concerns about whether ATR’s backlog (383 aircraft as of the end of 1H2023) could sustain this level of output for long.

Regional aircraft manufacturer commercial aircraft deliveries (2000-2023F*)

Source: CAPA – Centre for Aviation & company reports.

*2023 forecast based on manufacturer’s upper estimates.

Thanks to COVID-19, the dislocation of global supply chains, and own goals scored by OEMS: global aircraft deliveries are well below where they need to be to meet the ongoing growth in air travel demand. With deliveries short of where they should be, airlines are keeping older aircraft in service for longer – the global commercial airliner fleet is fewer in number and less efficient and capable overall.

If airlines are to meet air travel demand and improve their metrics in terms of efficiency, then the industry needs to be able to rely on OEMs to meet their delivery promises.